Types of regulated activity

Schedule 5 to the SFO stipulates 10 types of regulated activity and provides a detailed definition for each of them. These activities are:

- Type 1 Dealing in securities

- Type 2 Dealing in futures contracts

- Type 3 Leveraged foreign exchange trading

- Type 4 Advising on securities

- Type 5 Advising on futures contracts

- Type 6 Advising on corporate finance

- Type 7 Providing automated trading services

- Type 8 Securities margin financing

- Type 9 Asset management

- Type 10 Providing credit rating services

The definition of each type of regulated activity in Schedule 5 to the SFO is available at http://www.elegislation.gov.hk.

General requirements

Broadly speaking, you need a licence if you are not an authorized financial institution and:

{kind=link}

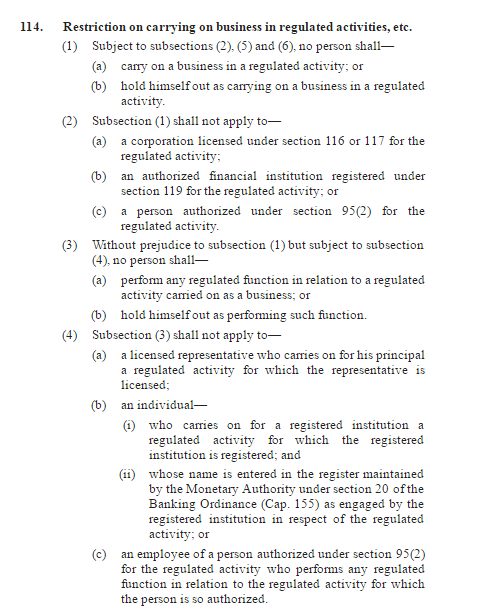

- you are a corporation carrying on a business in a regulated activity in Hong Kong (section 114(1) and (2) of the SFO);

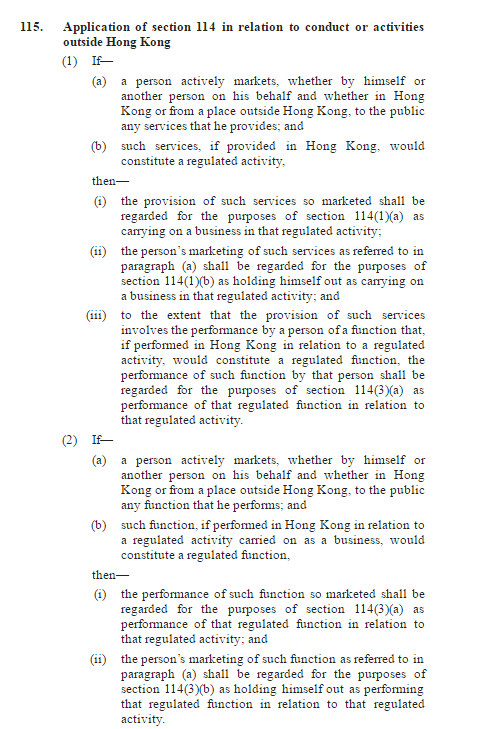

- you are a corporation actively marketing, whether by yourself or another person on your behalf and whether in Hong Kong or from a place outside Hong Kong, to the public any services that you provide, which would constitute a regulated activity if provided in Hong Kong (section 115 of the SFO)

See also FAQ ("Actively markets" under section 115 of the SFO); or

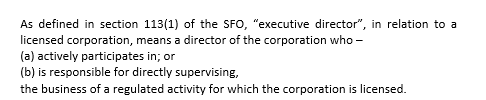

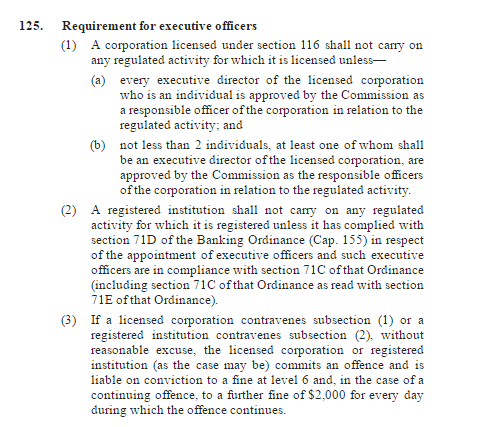

- you are an individual performing a regulated function for your principal which is a licensed corporation in relation to a regulated activity carried on as a business. In that case, you have to be a licensed representative accredited to your principal (section 114(3) and (4) of the SFO). In addition, if you are an executive director of that corporation, you also need to be approved as a responsible officer (section 125(1)(a) of the SFO).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You need a registration if you are an authorized financial institution and:

- you carry on a business of regulated activity other than Type 3 (leveraged foreign exchange trading) and Type 8 (securities margin financing) regulated activities. In that case, you have to be a registered institution (section 114(1) and (2) of the SFO); or

- you actively market, whether by yourself or another person on your behalf and whether in Hong Kong or from a place outside Hong Kong, to the public any services that you provide, which would constitute a regulated activity if provided in Hong Kong. In this case, you have to be a registered institution (section 115 of the SFO).

Relevant individuals who perform regulated functions in relation to regulated activities for registered institutions (e.g. bank staff working in the securities dealing department) are not required to be licensed or registered with the SFC. However, their names have to be entered in the register maintained by the HKMA if they are to perform regulated activities. That register is available on the HKMA’s web site (http://apps.hkma.gov.hk/eng/index.php).

Licensed corporations and registered institutions are referred to as “intermediaries”. Sole proprietorship or partnership is not an acceptable form of business structure for the purposes of licensing.

Exemptions

This part gives an overview of some situations in which exemption from the licensing requirements may apply under the SFO. You should refer to the SFO or consult your professional advisers if you need guidance specific to your case.

For simplicity, the terms “licence” and “licensed” in the rest of this page bear the same meaning as “registration” and “registered” respectively unless otherwise specified.

Incidental exemption

You may not be required to be licensed for certain regulated activities if such activities are performed wholly incidental to your carrying out of another regulated activity for which you are already licensed. Various factors are relevant in determining whether an incidental exemption is applicable to certain activity, for example whether the activity is subordinate to the carrying on of the other regulated activity for which the licensed corporation is or will be licensed, whether discrete fees are charged for the activity, and whether the activity constitutes a major part of the licensed corporation’s business. An incidental exemption may apply in the following circumstances:

Licensed for Type 1 regulated activity and carry out certain other regulated activities

You are licensed for Type 1 regulated activity (dealing in securities) and you wish to carry out Type 4 (advising on securities), Type 6 (advising on corporate finance) and/or Type 9 (asset management) regulated activity. You do not need to be licensed for Types 4, 6 and 9 provided that these activities are carried out wholly incidental to your securities dealing business. This exemption normally applies to stockbrokers who provide investment advice or manage discretionary accounts for their securities clients.

Licensed for Type 2 regulated activity and carry out certain other regulated activities

You are licensed for Type 2 regulated activity (dealing in futures contracts) and you wish to carry out Type 5 (advising on futures contracts) and/or Type 9 (asset management) regulated activity. You do not need to be licensed for Types 5 and 9 provided that these activities are carried out wholly incidental to your futures dealing business. This exemption normally applies to futures brokers who provide investment advice or manage discretionary accounts for their futures clients.

Licensed for Type 9 regulated activity and carry out certain other regulated activities

You are licensed for Type 9 regulated activity (asset management) and you wish to carry out Type 1 (dealing in securities), Type 2 (dealing in futures contracts), Type 4 (advising on securities) and/or Type 5 (advising on futures contracts) regulated activity. You do not need to be licensed for these regulated activities provided that they are carried out solely for the purposes of your asset management business (for Types 4 and 5, such asset management business must involve the management of a portfolio under a collective investment scheme). This exemption normally applies to fund managers who place trade orders to dealers or provide investment advice/research reports in the course of managing their own clients’ portfolios of securities and/or futures contracts.

Securities dealer - margin financier exemption

If you are licensed for Type 1 regulated activity (dealing in securities), you need not separately be licensed for Type 8 regulated activity (securities margin financing) to carry out securities margin financing activities for your clients. However, you would need to satisfy a more stringent financial resources requirement in terms of paid-up capital in order to do so (see Full licensed corporations > Specific approval criteria > Financial resources). This exemption normally applies to stockbrokers who also provide margin financing facilities to their securities clients.

Please note that in any event, authorized financial institutions are not required to be registered for Type 8 regulated activity to carry out securities margin financing activities.

Credit rating services

If you intend to prepare credit ratings for dissemination to the public or for distribution by subscription in Hong Kong or elsewhere, you are required to be licensed for Type 10 regulated activity.

However, if a firm prepares credit ratings only for its internal use, such as a bank’s internal systems for assessing counterparty risks, it is unlikely that the firm will be regarded as “providing credit rating services” for the purposes of the SFO because the credit ratings would neither be intended for dissemination to the public or distribution by subscriptions, whether in Hong Kong or elsewhere, nor reasonably expected to be so disseminated or distributed.

Similarly, a firm (such as a commercial credit reference agency) is unlikely to be required to be licensed for Type 10 regulated activity if it only gathers, collates, disseminates or distributes information concerning the indebtedness or credit history of any entity other than an individual. Consumer credit reference agencies are also excluded from the regulatory regime because the definition of “credit ratings” under the SFO excludes opinions regarding the creditworthiness of individuals.

See also FAQ (Credit rating agencies)

Dealing with professional investors exemption

You may not be required to be licensed for futures or securities dealing activity if you act as principal and deal with professional investors only. This exemption will apply if:

{kind=link}

In relation to dealing in futures contracts

- you as principal carry out the dealing activity concerned in relation to a futures contract traded other than on a recognized futures market as defined in Schedule 1 of the SFO by way of dealing with a person who is a professional investor (whether acting as principal or agent); or

In relation to dealing in securities

- you as principal carry out the dealing activity concerned by way of dealing with a person who is a professional investor (whether acting as principal or agent).

Group company exemption

You are not required to be licensed for Type 4 (advising on securities), Type 5 (advising on futures contracts), Type 6 (advising on corporate finance) or Type 9 (asset management) regulated activity if you provide the relevant advice or services solely to your wholly owned subsidiaries, your holding company which holds all your issued shares, or other wholly owned subsidiaries of that holding company.

In relation to advisory activities

The exemption should not be applied to a corporation advising its group company in respect of that group company’s client assets. However, where the investment advice and/or related research reports are provided to the group company for its own consumption, notwithstanding that the group company may rely, in whole or in part, on such advice/research reports to service its clients, the above exclusion will still apply if the advice/research reports are issued to the clients by the group company in its own name and that group company has assessed the corporation’s input before issuing such advice/research reports.

In relation to asset management activities

The exemption is only applicable to a corporation providing asset management service to its group company (on a wholly owned basis) in respect of that group company’s assets. It should not be read as applying to the management of assets belonging to the group company’s clients. Managing assets belonging to third parties would constitute “asset management” and attract a licensing requirement.

Professional exemption

If you are a solicitor, a counsel or a professional accountant, you are not required to be licensed for Type 4 (advising on securities), Type 5 (advising on futures contracts), Type 6 (advising on corporate finance) or Type 9 (asset management) regulated activity if you provide such advice or services wholly incidental to your practice as a solicitor, a counsel or a professional accountant.

Broadcaster/Journalist exemption

If you give advice on securities, futures contracts or corporate finance or issue related analyses or reports through:

- a newspaper, magazine, book or other publication which is made generally available to the public; or

- television broadcast or radio broadcast for reception by the public, whether on subscription or otherwise,

you are not required to be licensed for Type 4, Type 5 or Type 6 regulated activity (as the case may be).

Trust company exemption

In relation to dealing in securities

If you are a trust company registered under Part VIII of the Trustee Ordinance, you are not required to be licensed for Type 1 regulated activity (dealing in securities) if you act as an agent for a collective investment scheme to distribute application forms, redemption notices, conversion notices and contract notes, and/or receive money and issue receipts on behalf of your principal.

In relation to investment advisory activities

As a trust company, you are not required to be licensed for Type 4 (advising on securities), Type 5 (advising on futures contracts), Type 6 (advising on corporate finance) or Type 9 (asset management) regulated activity if you provide such investment advice or services wholly incidental to your discharge of your duty as a trustee.

In relation to asset management activities

If a trustee company acting as trustee of a discretionary trust has appointed an appropriate person to manage the portfolio or in practice acts on professional advice in carrying out its duties as trustee, it would not be required to be licensed. However, if the provision of portfolio management services becomes a separate or distinct business of the trustee company, it is unlikely that the trustee company could rely on the wholly incidental exemption and it would have to apply for a licence for Type 9 regulated activity.

Leveraged foreign exchange trading exemption

Schedule 5 to the SFO provides a number of exclusions in the definition of “leveraged foreign exchange trading”. For example, if you are an authorized financial institution, you are not required to be registered for Type 3 regulated activity (leveraged foreign exchange trading) in order to carry out such activity.

The Securities and Futures (Leveraged Foreign Exchange Trading – Exemption) Rules set out the requirements and conditions in applying the exemption provided in paragraph (xiii) of the definition of “leveraged foreign exchange trading” of Schedule 5 to the SFO. Please refer to the relevant provisions for details.

Further guidance

Conducting business outside Hong Kong

A licence is issued by the SFC under Part V of the SFO only to allow the holder to carry on business in a regulated activity, or to perform a regulated function in relation to a regulated activity carried on as a business, in Hong Kong. When a licensed corporation or individual conducts activities in a jurisdiction outside Hong Kong, it is necessary for such corporation or individual to ensure that the relevant legal and regulatory requirements of that other jurisdiction are fully complied with.

Financial technology (Fintech)

SFC Regulatory Sandbox

Firms demonstrating a genuine and serious commitment to carry on regulated activities through the use of innovative Fintech may operate regulated activities in a confined regulatory environment (i.e. the SFC Regulatory Sandbox). In order to contain risks to investors, the SFC may impose licensing conditions on qualified firms upon licensed, and place them under closer monitoring and supervision when they operate in the Sandbox.

See also "Circular to announce the SFC Regulatory Sandbox".

Virtual asset fund managers

Firms which intend to manage portfolio(s) with composition of more than 10% of virtual assets are expected to comply with additional expected regulatory standards. The expected additional regulatory standards will be imposed by way of licensing conditions that refer to a set of Terms and Conditions.

See also “Statement on regulatory framework for virtual asset portfolios managers, fund distributors and trading platform operators” and its appendice on “Regulatory standards for licensed corporations managing virtual asset portfolios” and “Conceptual framework for the potential regulation of virtual asset trading platform operators”

Virtual asset fund distributors

Firms which distribute funds that invest (solely or partially) in virtual assets in Hong Kong are required to be licenced for Type 1 regulated activity (dealing in securities). Given the significant risks posed to investors, guidance on the expected standards and practices when distributing virtual asset funds is provided in the "Circular to intermediaries on the distribution of virtual asset funds".

Virtual asset trading platforms

In 2019, the SFC introduced a regulatory framework for virtual asset trading platforms. Centralised platforms which provide virtual asset trading services and intend to offer trading of at least one security token may apply to the SFC for a licence for Type 1 (dealing in securities) and Type 7 (providing automated trading services) regulated activities.

See also “Position paper on regulation of virtual asset trading platforms”

Security token offerings

In Hong Kong, security tokens are likely to be “securities” as defined in the SFO and so are subject to the securities laws of Hong Kong. Where security tokens are "securities", unless an applicable exemption applies, any person who markets and distributes security tokens (whether in Hong Kong or targeting Hong Kong investors) is required to be licensed for Type 1 regulated activity (dealing in securities) under the SFO.

See also “Statement on security token offerings”

Bitcoin Futures

Bitcoin Futures traded on and subject to the rules of conventional exchanges are regarded as “futures contracts” under the SFO. Accordingly, parties carrying on a business in dealing in such Bitcoin Futures are required to be licensed for Type 2 regulated activity (dealing in futures contracts) under the SFO.

Provision of financial information on the internet

Periodical publication exemption

The definitions of “advising on corporate finance”, “advising on securities”, and “advising on futures contracts” in Schedule 5 to the SFO provide a specific exclusion for a person giving advice through a newspaper, magazine, book or other publication which is made generally available to the public (see Exemptions > Broadcaster/Journalist exemption). Internet publications may rely on this licensing exemption if they are able to satisfy the requirements of the provisions.

Providing generic factual market information

The ambit of “advising on securities” or “advising on futures contracts” as defined in Schedule 5 to the SFO is broad. In the present context, the licensing requirement should not generally be extended to cover activities concerned solely with the provision of generic factual market information (whether or not through the Internet) where no recommendation on specific securities/futures contracts or investment advice has been made, or to cover the reproduction of the entire research reports of persons licensed by or registered with the SFC.

Providing analytical tools

Analytical tools facilitating the making of investment decisions are often available from financial information web sites. In general, where the tools are able to identify a variety of investment possibilities or recommendations presenting different choices to users, the providers of such tools would be regarded as “advising on securities” or “advising on futures contracts”. An example would be an analytical tool able to make specific recommendations on the basis of the investment profile (such as risk aversion, age or projected cash flow) as determined by the user. However, the mere provision of analytical tools which solely filter publicly available data in a transparent process does not constitute an advisory activity. For example, the provision of a computer programme that identifies stocks of a particular industry sector having price earning ratios below a predetermined level, or that identifies investment funds having past annual returns above a predetermined level, should not trigger a licensing requirement.

Provision of on-line services

Hyperlinks to other financial web sites

The mere presence of hyperlinks, notwithstanding the links may be with a licensed or registered person, does not of itself trigger a licensing requirement. However, the presence of any inducement, or invitation, to visit the related sites through the links concerned may mean a licence or registration is required. It should be noted that effecting an introduction of a client to a securities/futures/leveraged foreign exchange dealer or its representative in return for a commission, rebate or other remuneration may constitute a regulated activity, for which a licence or registration may be required.

Providing automated trading services (ATS)

A corporation that provides automated trading services (ATS) as defined in Schedule 5 to the SFO shall either be authorized to provide ATS under Part III of the SFO, or licensed or registered under Part V of the SFO. As a general practice, if that corporation is already an intermediary in respect of other type(s) of regulated activity, it would need to be licensed or registered for Type 7 under Part V of the SFO. An intermediary wishing to submit such application should first read the “Guidelines for the Regulation of Automated Trading Services” and consult its professional advisers on related business proposal where necessary.

Order routing facilities

It should be noted that the provision of electronic order routing facilities and online facilities that simply allows clients to register for monthly subscription plans of authorized collective investment schemes or transmit regular subscription and redemption orders generally would not be regarded as Type 7 regulated activity. If an intermediary intends to conduct dealing activities in the form of the above facilities via the Internet, it is required to:

- complete and submit a Questionnaire for Providing Electronic Trading Services in Questionnaire 2; and

- notify the SFC in writing the effective date of launching such internet services and the address of the web site.

An intermediary is responsible for ensuring that the order routing services or other electronic services that it wishes to provide do not fall within the definition of “providing ATS” under Schedule 5 to the SFO. If the services do fall within the definition, the intermediary would need to be licensed or registered for Type 7 regulated activity (as the case may be).

Financial training

An SFC licence is generally not required for providing financial training or sharing general investment knowledge (e.g. in a classroom setting or through the internet). However, if the instructor or website digresses from imparting general investment knowledge to recommending specific stocks to students/viewers or inducing them to trade securities, the training institution, instructor and/or website content provider may be required to hold SFC licences.

Promotional or incentive schemes

Intermediaries offering promotional schemes organized in conjunction with their affiliates should pay special attention to the licensing requirements. In particular, care should be taken to ensure that the marketing activities do not cause the affiliates (which may not be licensed or registered) to engage in dealing in securities, dealing in futures contracts or other regulated activities.

The implementation of incentive schemes, whereby any member of the public (as conducting a business himself) would be remunerated in the form of commission, rebate, etc. after successfully introducing clients to a licensed person or a registered institution, is generally unacceptable. Such practice could potentially result in the introducing party engaging in unlicensed regulated activities. The licensed person or registered institution concerned could also be liable for aiding and abetting the offence. It is of concern that the clients so introduced may not receive the appropriate protection afforded by the regulatory regime. In addition, the introducing party may not be fit and proper to carry out that function.

Private equity and venture capital firms

The term "securities" is given a wide definition in Schedule 1 to the SFO. However, shares or debentures of a company that is a private company within the meaning of section 11 of the Companies Ordinance (Cap. 622) is excluded from the definition. As such, a firm that deals in, advises on or manages a portfolio of “private equity” or “venture capital” which does not involve securities may not by itself attract a licensing requirement. In many other cases, however, where a firm deals in, advises on or manages shares or debentures of private offshore companies that fall outside the definition of “private company” under the Companies Ordinance, it is likely that the firm in question will be required to be licensed.

{kind=link}

Depending on a firm’s business model, it may be required to be licensed to carry on one, or more than one, type of regulated activity. As a general guidance:

- if a firm is delegated with discretionary power to make investment decisions on securities for a fund in Hong Kong, it is required to obtain a licence for Type 9 regulated activity (asset management);

- if a firm has not been granted any discretionary investment authority by the fund it serves, it may still need to be licensed for the following types of regulated activities:-

- Type 1 regulated activity (dealing in securities) for marketing or distributing a fund or conducting any other securities dealing activities (e.g. deal negotiation and trade execution) for the fund;

- Type 4 regulated activity (advising on securities) for providing advice in respect of the investments or prospective investments of the fund.

Please also refer to the above sections regarding incidental exemption.

See also “Circular on private equity firms seeking to be licensed”

Inter-dealer brokers

The obligation of inter-dealer brokers to be licensed under the SFO is largely dictated by the nature of the financial instruments that they trade, their clients and the booking structures which they employ. However, it is likely in most cases that inter-dealer brokers are carrying on a business in Type 1 regulated activity (dealing in securities), Type 2 regulated activity (dealing in futures contracts) and/or Type 3 regulated activity (leveraged foreign exchange trading). If an inter-dealer broker is conducting any of these activities, it must be appropriately licensed under the SFO unless it is able to rely upon any of the exemptions stipulated in the SFO.

Investment-Linked Assurance Schemes (ILAS)

As a general rule, the SFC considers that insurers, corporate insurance brokers and insurance intermediaries who are dealing solely in ILAS and other insurance products should not be licensed under the SFO. However, slight variations in circumstances can result in different interpretations of statutory provisions. In the event of an insurer, a corporate insurance broker or an insurance intermediary engages in regulated activities within the meaning of the SFO, an obligation to be licensed under the SFO might well arise.

Licensing of compliance officers/in-house counsel

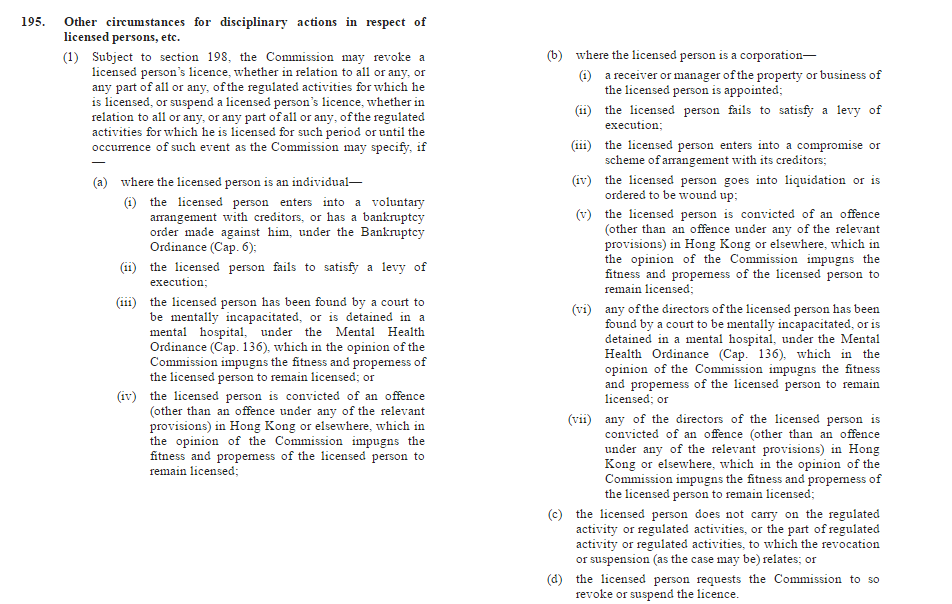

Normally, the SFC will not license back office staff, including compliance officers and in-house legal counsel, if s/he does not perform functions that directly relate to the conduct of the regulated activity for which the corporation is licensed. If a licensed individual becomes a back office staff by reason of a change of position within the firm, s/he should request a revocation of her/his licence forthwith under section 195(1)(d) of the SFO.

{kind=link}

As a matter of general principle, the SFC considers it necessary for there to be segregation between the performance of compliance or legal function and the performance of the activities that constitute the carrying on of regulated activities. Without such segregation, there would be inherent conflict arising out of a compliance officer or in-house legal counsel carrying on the regulated activities for which the corporation employing him/her is licensed and, at the same time, being responsible for supervising such activities for the purposes of regulatory compliance.

Exercise of discretionary investment authority for Type 9 regulated activity

Under Schedule 5 to the SFO, Type 9 regulated activity (asset management) means “real estate investment scheme management” or “securities or futures contracts management”. For any corporation that would like to be licensed for Type 9 regulated activity (asset management), the SFC generally expects such corporation to be able to exercise discretionary investment authority to make investment decisions for its clients. Such discretionary investment authority must be properly delegated to the corporation.

Family Offices

The licensing regime under the SFO is activity-based. If the services provided by a family office do not constitute any regulated activity or they fall within any of the available carve-outs, the family office is not required to be licensed under the SFO. However, family offices should take care not to hold themselves out as carrying on a business in a regulated activity without a licence.

For example, a family appoints a trustee to hold its assets of a family trust, and the trustee operates a family office as an internal unit to manage the trust assets, the single family office will not need a licence because it will not be providing asset management services to a third party.

A company or family office set up as a business to manage assets which include securities or futures contracts may be required to hold a licence for Type 9 regulated activity (asset management). If a family office intends to provide other services such as acquiring financial assets following instructions made by the family, it should review whether they fall within the definition of any of the other types of regulated activities such as Type 1 (dealing in securities) and whether it is required to be licensed for them.

See also “Circular on the licensing obligations of family offices”

Custodian of private Open-ended Fund Companies

An intermediary which is licensed or registered for Type 1 regulated activity (dealing in securities) may act as a custodian of private Open-ended Fund Companies (OFC) provided that it meets the eligibility requirements set out in 7.1(b) of the Code on Open-Ended Fund Companies (OFC Code). Among other things, the intermediary’s licence or registration should not be subject to any condition that it shall not hold client assets. Where the intermediary is a licensed corporation, it should also satisfy the additional financial resources requirements. The intermediary should comply with all relevant requirements, including those set out in Appendix A to the OFC Code regarding the safekeeping of OFC scheme property. The SFC may impose a condition on the intermediary’s licence or registration to the effect that it must comply with all requirements applicable to it as a custodian of an OFC.

See also “Circular on implementation of changes to the open-ended fund companies regime” and “FAQs relating to OFC” (Question 6A) regarding required documents to be submitted

Last update: 9 Feb 2022